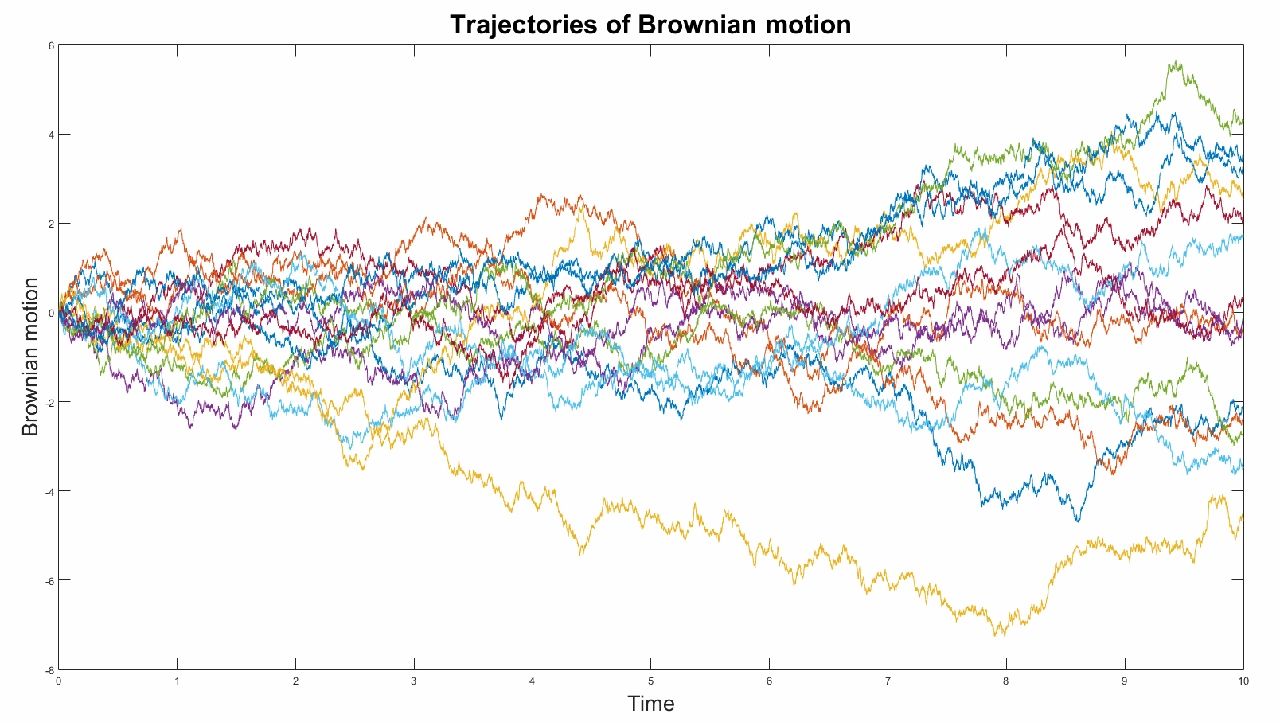

Differentiable Brownian Motion Kantorovich Calculus - We will later see that on a suitable (ω,a,p) we can construct a brownian motion. Brownian motion is almost surely nowhere differentiable. Specif ically, p(∀ t ≥ 0 : This course gives an introduction to brownian motion and stochastic calculus. Even a continuous stochastic process can be nowhere differentiable.

Even a continuous stochastic process can be nowhere differentiable. This course gives an introduction to brownian motion and stochastic calculus. Specif ically, p(∀ t ≥ 0 : Brownian motion is almost surely nowhere differentiable. We will later see that on a suitable (ω,a,p) we can construct a brownian motion.

Brownian motion is almost surely nowhere differentiable. Even a continuous stochastic process can be nowhere differentiable. This course gives an introduction to brownian motion and stochastic calculus. Specif ically, p(∀ t ≥ 0 : We will later see that on a suitable (ω,a,p) we can construct a brownian motion.

Statistics & Finance Tutor Brownian Motion in R, Matlab, SAS New

We will later see that on a suitable (ω,a,p) we can construct a brownian motion. Specif ically, p(∀ t ≥ 0 : Even a continuous stochastic process can be nowhere differentiable. Brownian motion is almost surely nowhere differentiable. This course gives an introduction to brownian motion and stochastic calculus.

Brownian motion calculus

Even a continuous stochastic process can be nowhere differentiable. Brownian motion is almost surely nowhere differentiable. Specif ically, p(∀ t ≥ 0 : This course gives an introduction to brownian motion and stochastic calculus. We will later see that on a suitable (ω,a,p) we can construct a brownian motion.

Brownian motion PPT

This course gives an introduction to brownian motion and stochastic calculus. We will later see that on a suitable (ω,a,p) we can construct a brownian motion. Specif ically, p(∀ t ≥ 0 : Brownian motion is almost surely nowhere differentiable. Even a continuous stochastic process can be nowhere differentiable.

(PDF) Fractional Brownian motion as a differentiable generalized

Specif ically, p(∀ t ≥ 0 : Brownian motion is almost surely nowhere differentiable. Even a continuous stochastic process can be nowhere differentiable. This course gives an introduction to brownian motion and stochastic calculus. We will later see that on a suitable (ω,a,p) we can construct a brownian motion.

The Brownian Motion an Introduction Quant Next

We will later see that on a suitable (ω,a,p) we can construct a brownian motion. This course gives an introduction to brownian motion and stochastic calculus. Even a continuous stochastic process can be nowhere differentiable. Brownian motion is almost surely nowhere differentiable. Specif ically, p(∀ t ≥ 0 :

208 Brownian Motion Symmetric Random Walk Stochastic Calculus for

Brownian motion is almost surely nowhere differentiable. Even a continuous stochastic process can be nowhere differentiable. Specif ically, p(∀ t ≥ 0 : This course gives an introduction to brownian motion and stochastic calculus. We will later see that on a suitable (ω,a,p) we can construct a brownian motion.

8 Brownian Motion Examples in Real Life StudiousGuy

Even a continuous stochastic process can be nowhere differentiable. This course gives an introduction to brownian motion and stochastic calculus. Specif ically, p(∀ t ≥ 0 : We will later see that on a suitable (ω,a,p) we can construct a brownian motion. Brownian motion is almost surely nowhere differentiable.

Brownian motion PPT

Brownian motion is almost surely nowhere differentiable. Specif ically, p(∀ t ≥ 0 : This course gives an introduction to brownian motion and stochastic calculus. We will later see that on a suitable (ω,a,p) we can construct a brownian motion. Even a continuous stochastic process can be nowhere differentiable.

brownianmotionstochasticcalculus

We will later see that on a suitable (ω,a,p) we can construct a brownian motion. Even a continuous stochastic process can be nowhere differentiable. Specif ically, p(∀ t ≥ 0 : Brownian motion is almost surely nowhere differentiable. This course gives an introduction to brownian motion and stochastic calculus.

Kantorovich Variational Method For Buckling of SSSS Plate PDF

Brownian motion is almost surely nowhere differentiable. This course gives an introduction to brownian motion and stochastic calculus. Specif ically, p(∀ t ≥ 0 : Even a continuous stochastic process can be nowhere differentiable. We will later see that on a suitable (ω,a,p) we can construct a brownian motion.

This Course Gives An Introduction To Brownian Motion And Stochastic Calculus.

Brownian motion is almost surely nowhere differentiable. We will later see that on a suitable (ω,a,p) we can construct a brownian motion. Specif ically, p(∀ t ≥ 0 : Even a continuous stochastic process can be nowhere differentiable.